Increased Price Transparency Could Shake up the Hong Kong Personal Loan Markets

Loyalty takes several different forms and the multitude of factors influencing it can make it difficult to measure: there’s loyalty of convenience, when the logistics of changing providers outweigh the expected benefits of doing so; loyalty of compensation, when the benefits offered by one provider outweigh the negative experiences inherent in dealing with them; and loyalty of association, loyalty in its best form, when the customer values the relationship more than the product.

In this article I’m going to take a simplified look at where loyalty in one of these three forms exists when a consumer applies for a new loan with the same lender they took out previous last loan.

Price helps determine loyalty — but not necessarily how you think

When we think about a simple definition of loyalty, there are a few pieces of conventional wisdom we might refer to: young borrowers are expected to be less loyal, having had less time to establish firm relationships; borrowers of short-term loans are expected to be more loyal, since the cost of higher rates have less time to compound; and higher-risk borrowers are expected to be more loyal, with fewer lenders willing to make them an offer

These expectations are to some degree reflected reflect in the data we have. Younger borrowers are less loyal than older borrowers, shorter-term borrowers are more loyal than longer-term borrowers, and higher-risk borrowers are less loyal. However, several of those factors are over-lapping, so when we control for factors like term and risk, we see that the difference in loyalty between older and younger borrowers flatten.

There are several factors that influence a borrower’s propensity to reapply for a loan at the same lender, and one would think the price of the loan played the biggest role when influencing loyalty. And to some extent that is true — the rate at which loans are booked at a new lender increases as the price of those loans moves further away from the average. What is interesting, though, is which average acts as a determining factor.

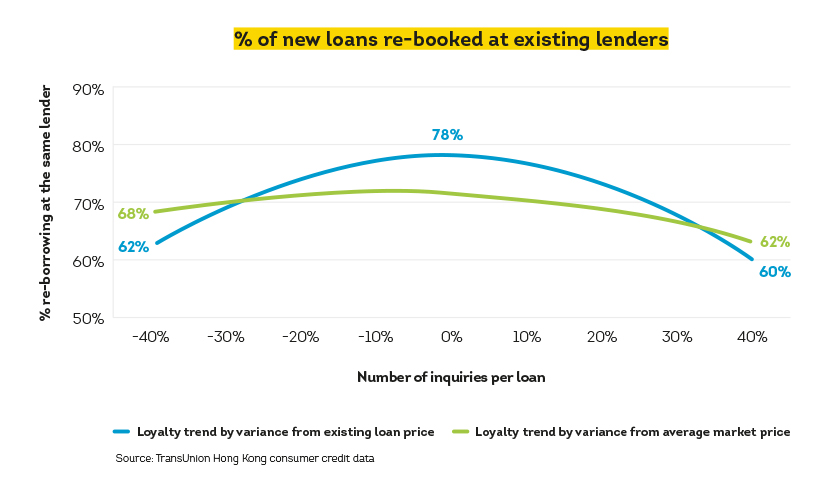

In a completely transparent market, we would expect a consumer to deem an offered rate as fair or unfair based on how far it was from the going rate. To measure if this was the case, I first calculated an average annual percentage rate (APR) for loans booked per risk tier and term combination as a stand-in for the going rate. I then calculated the rate at which new loans were rebooked with existing lenders depending on how far away from that average that loan’s price was set.

A U-shaped trend emerged which supports our expectations, but only slightly so. When the new loan is booked at or near the going market rate, 71% of loans are booked at the same lender where the customer took out their most recent loan, dropping into the 60% range as the variance grows.

However, when we did the same calculation with the baseline set as the customer’s previous loan’s price, the U-shaped loyalty curve that emerged was much steeper. Now, when the new loan is booked at or near the price of the most recent loan, 78% of loans are booked with the same lender where the customer took out that most recent loan, dropping even deeper as the variance grows

This suggests that consumers pay more attention to the price of their most recent loan than the going rate. Or, more likely, they simply don’t know what the going rate is. If their risk profile hasn’t changed significantly from when that previous loan was taken out, this is not a problem, the two reference rates will be similar. But many loan customers see their scores change significantly over times and those consumers could be paying more than they need to.

Why do borrowers allow this to happen? And what does it mean for lenders?

How to manage the shift towards price transparency

In part, at least, the situation exists because consumers don’t shop around. Half of all consumers make only one loan inquiry per new loan opened while three-quarters make no more than two — and many of those who do shop around pose a higher risk, suggesting their search for options might be out of necessity instead of choice.

As for what it means for lenders, the ability to retain customers is currently being helped by a general lack of price awareness. However, there is about to be an injection of new virtual lenders and one common trend that FinTechs bring to any market is an increase transparency

For now, it may be sufficient to price your loans in line with historic loans you’ve provided to the customer, relying on loyalty of convenience. Eventually your focus will have to shift to ensure your competitive prices are more transparent to foster loyalty of compensation. To do this, lenders will have to appear in centralised marketplaces with embedded strategies and consider employing more targeted direct marketing programmes that reveal the competitive price before the customer has to go through the steps of actually applying.

This leaves the question of loyalty of association, which I’ll address in more detail in my next article. As for the concept of loyalty itself, the ‘better experience’ we expect to drive this is too nuanced to be fully explored in credit data alone. That said, loan turnaround times are a reasonable proxy for the ease of opening a loan and we do see that lenders with faster turnaround times tend to earn higher APRs for loans of a given size and risk.

Borrowers may well be willing to pay extra to lenders who have invested in better loan origination strategies and possibly lenders who invest in a more user-friendly experience in general.

LEARN MORE

For more insights into the Hong Kong consumer credit market, read TransUnion’s latest quarterly Industry Insights Report and other articles here.

Business Contact Us

We're sorry, your request failed. Please try again in a little while.